Overview

MINT students gain real-life exposure to the SDG trillion-dollar agenda

Post pandemic, the global estimated funding required to achieve the ambitious agenda of the 2030 Sustainable Development Goals was revised to 4.2 trillion USD per year, a 40% increase compared to pre-pandemic. The question remains: where will this funding come from? What are the roles that the public and respectively the private sector play in this effort and how? What are some of the key opportunities and challenges associated with financing SDG-aligned enterprises and other efforts? How can governments unlock the scale of capital allocation needed to achieve the SDGs?

“Financing the SDG Agenda: Unpacking the Trillion Dollar Opportunity” is a highly interactive course part of the MINT program hosted by Visiting Lecturer Brindusa Burrows. It is designed to introduce students to types of actors, mechanisms, strategies and opportunities available to public and private financing institutions. In autumn 2021, students were able to dive into a range of concrete investment thematics and discuss SME finance, particularly in emerging markets, a timely and important issue particularly in the aftermath of the COVID-19 pandemic. with guest experts including Jennifer Blanke (ex VP African Development Bank), James Cameron (Pollination, UK), Valerie Harrington (Blue Orchard, Switzerland), David Taylor (Cardano Foundation, Switzerland), Christine Coignard-Haas (BoD member Eramet, France), Xavier Pierluca (Enabling Qapital, Switzerland), Almira Cemmel (FTI, UK) and Kostis Tselenis (Swiss Impact Office).

Students worked in groups on real-life projects, solving relevant and cutting-edge current research questions in partnership with key external organizations highly active in the space of SDG finance. Several groups were invited to present their findings directly to the company leadership and all students received inspiration for their future careers. Several groups summarized the results of their research, available below.

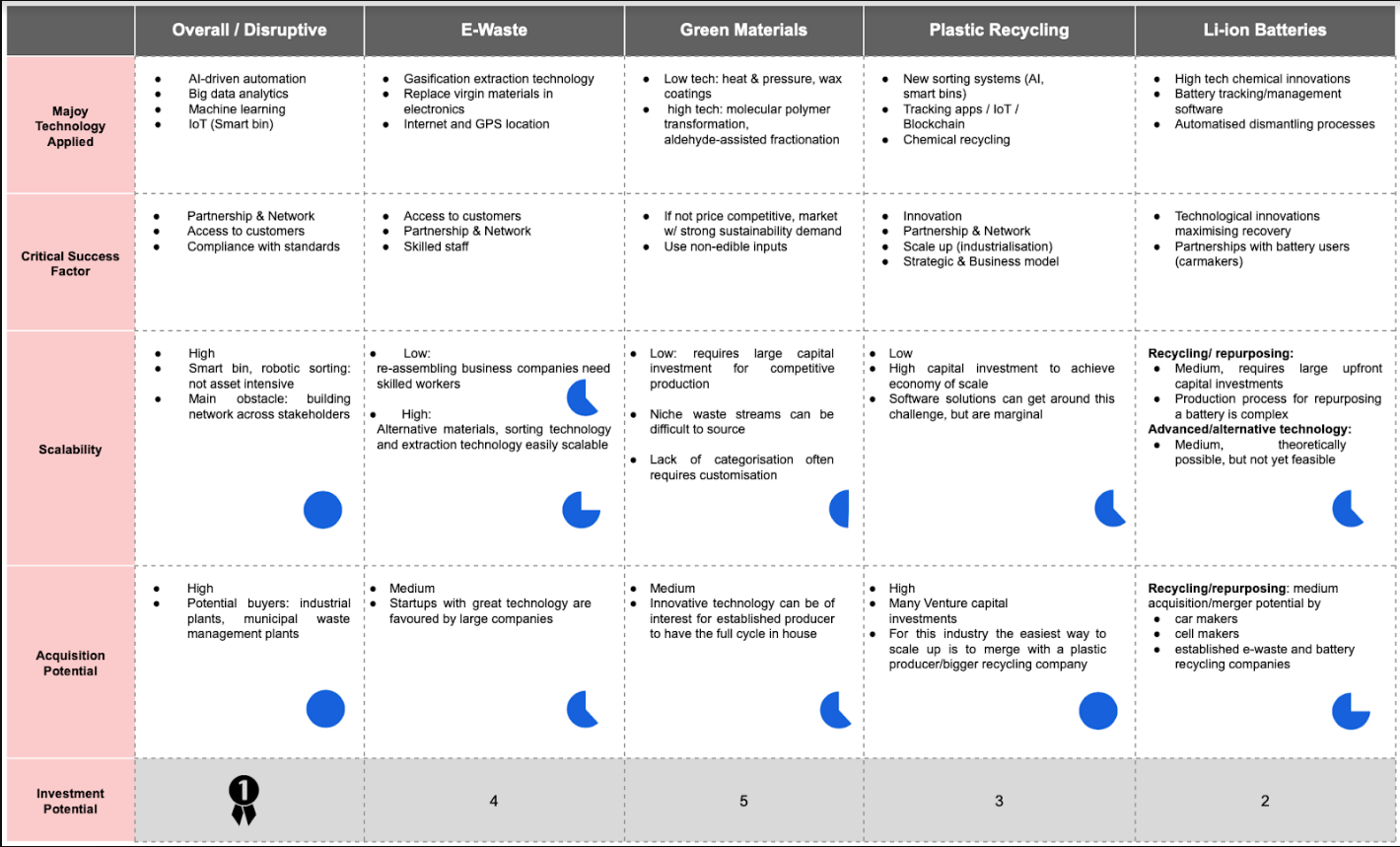

Group 1: Deep dive into smart recycling and clean/green materials in Switzerland working with Swisscom Venture Capital. The group provided incisive market research and received accolades from the group’s sustainability-focused Investment Director, Jennifer Webb.

Group 2: Carbon credit financing analysis of landscape working with Enabling Qapital. The group worked closely with Xavier Pierluca, Managing Partner of the impact asset management firm, and their research was presented to the firm leadership.

Groups 3-5: Country market studies: Nigeria, Morocco, and Indonesia working with Ground Up Project. The groups identified key economic sectors linked to the achievement of the SDGs, including challenges and opportunities to invest in the country. The group working on key SDG-related opportunities in Morocco had their thorough work appraised by CEO Brindusa Burrows and the senior leadership of Ground Up Project.

Group 6: European Green Deal financing for Romania, with Raiffeisen Romania. Students provided the bank with detailed research on the diverse sources of finance available in relation to the Green Deal. Their work was highlighted by the Executive Director, Regional Corporate and Public Sector Raiffeisen Romania, Radu Ciocoiu.

Group 7: Leveraging private funding for the SDGs, with the Sanitation and Hygiene Fund. Students worked very closely with the newly appointed head of the fund – Dominic O’Neill – and SHF Board member Jennifer Blanke on strategies for differentiation and leveraging private foundations money into the fund’s new structure and its thematic. Their research was embedded in the strategy presentation made by the SHF to its board.